Easmond Tsewole

Chief Executive Officer

An AI analysis of the financial ratios and metrics of high growth credit unions, based on XGBoost trained on of 5 years of quarterly call report data

Mostpeer benchmarking quietly assumes:

“What works for a $400M credit union should basically work for a $2B credit union.”

Our data says that’s wrong.

We trained a AI Models (XGBoost classification models) on five years of quarterly NCUA call report data, segmenting credit unions into three asset tiers and comparing:

Across cohorts, our models were able to predict whether a credit union was a Fast Growing Credit Union, vs Slow Growing with a 74%-81% accuracy, with only looking at their financial ratios & metrics.

Here are the top three drivers of growth by tier, ranked by feature importance (share of total model gain):

Same industry. Same regulator. Completely different recipes.

Under $500M in total assets, fast growers win on:

At this size, you don't win by out-spending anyone, you win by:

If you're under $500M and your accounts per member and member YoY growth is flat, it's worth prioritizing deepening relationships with members. The credit unions with deeper relationships tended to grow faster than those with more breadth.

Between $500M and $1B, the story flips. The top two drivers are:

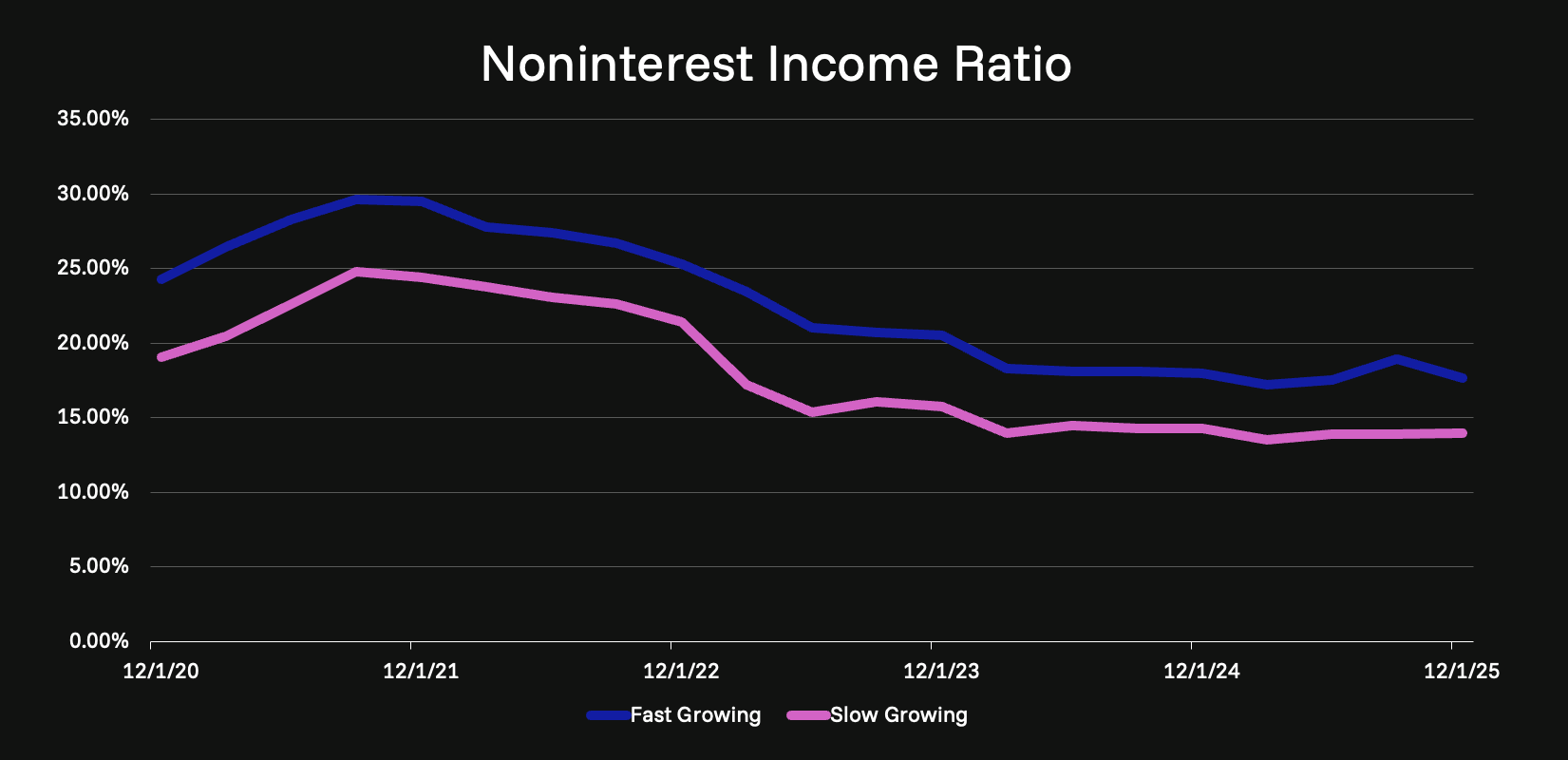

Together they account for 16.5% of total feature importance, the most concentrated signal in any model we ran. Noninterest Income Ratio is still there, but it’s downstream of cost discipline.

Fast growers in this band are not just selling more. They are:

This is the make‑or‑break tier. You either convert prior relationship wins into operating leverage, or you get stuck with big‑credit‑union costs and small‑credit‑union economics.

At $1B and above, the mix changes again. The leading signals:

Large fast‑growing CUs are running franchises, not just balance sheets:

At this level, growth is about orchestrating mix, cost, and credit quality, not just “more loans.”

Across all three asset tiers, Noninterest Income as a % of Total Income ranks in the top three. At the $1B+ tier, it is the single most important variable in the model, contributing 10.4% of total importance, nearly double the typical feature.

But the interpretation matters:

So the leadership question isn’t:

“Is our noninterest income ratio high?”

It is:

“Is our noninterest income ratio where it is because we’re growing assets smartly, or because we’re failing to drive product usage and fee‑based engagement?”

Same number, two completely different diagnoses.

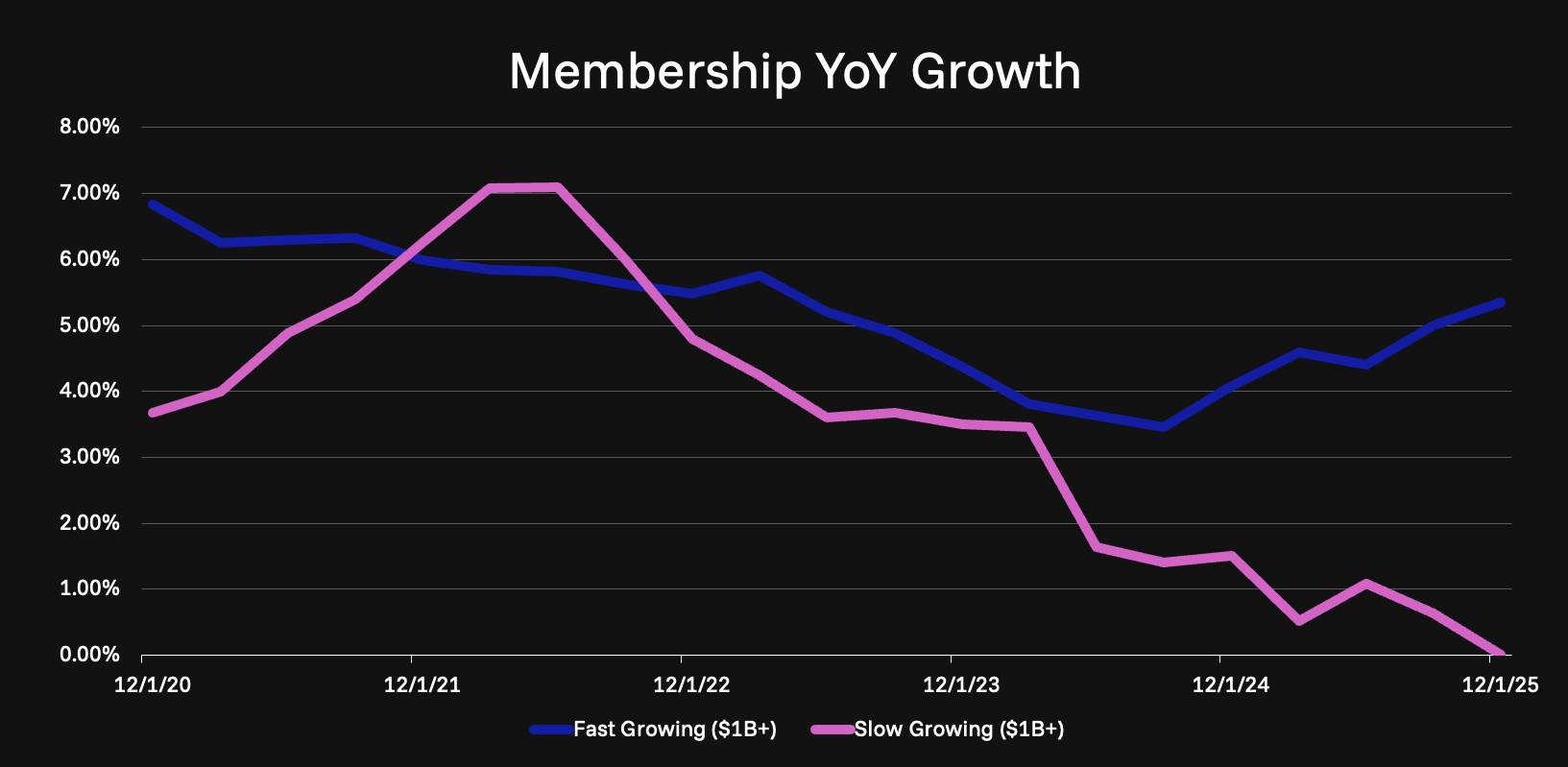

While noninterest income gets the headline, year-on-year membership growth (Members YoY) shows up near the top in every tier:

Net member growth is non‑negotiable for fast growers across the industry.

Member growth is also one of the few metrics that’s almost impossible to financially engineer. You either acquired net new members this year or you didn’t. The fact that it surfaces across all three models says: organic member acquisition is a prerequisite for asset growth, not a substitute for it.

For mid‑market and large credit unions, the models are blunt:

Fast‑growing larger CUs aren’t just selling more. They are:

That combination is what gives them the capacity to keep reinvesting in products, technology, and growth without eroding net worth.

Just as informative as the top features are the ones at the bottom. Across all three models, these consistently ranked in the bottom five:

Two implications:

Don’t overcomplicate this. Build a tier‑appropriate scorecard and plot your last 5 years against fast‑ and slow‑grower averages in your band.

If you’re under $500M, focus on:

If you’re $500M–$1B, focus on:

If you’re $1B+, focus on:

If your line looks more like the slow-grower cohort, strategic adjustments shou

Every credit union wants to grow. But what actua

wer change depending on your size?

To find out, we trained an AI model on five years of NCUA call report data across 4,015 credit unions. We asked a simple question: can we predict which credit unions will grow their assets faster than 6% annually, using only their financial ratios?

The answer was yes, with 70% to 80.6% accuracy depending on the cohort. But the more interesting finding was what the model learned along the way. The features that predict fast growth at a $200M institution are not the same features that predict fast growth at a $1B institution.

The playbook changes as you scale.

A final note on benchmarking: features that look important in industry‑wide analyses (like Share Draft Penetration) often fall to mid‑pack importance once you control for asset tier. The drivers of growth in your tier are not the drivers of growth in the tier above or below you.

Benchmark within your tier, not against the industry average. The credit unions winning the growth race are leaving a clear trail in their ratios. Your job as an executive is to decide whether you’re willing to let that trail change what you work on next.

Perspective for technical leaders navigating growth and strategy, while being secure & compliance.