Easmond Tsewole

Chief Executive Officer

The last five years of credit uniongrowth ran on two engines, funding and deployment. What does the next 5 yearslook like, what trends can we anticipate, and what engines will propel the topcredit unions’ growth?

The last five years saw three distinct operating periods. Most credit unions were built for one of them.

2020–2021 the covid liquidity flood. Stimulus check and PPP loan deposits swelled. Mortgage and refinancing activity grew. Funding was effectively free. Auto loan volumes, particularly new auto were impacted by reduced demand, then supply chain constraints, before recovering.

2022–2023 was the rate shock. The Federal Funds Target Rate Ranges went from 0%-0.25% to 5.25%- 5.50% in 18 months. Members moved money to brokerages, treasuries, and high-yield online banks to take advantage of the higher rates. The credit unions that adapted fastest were the ones that learned to compete on rate for share certificates.

2023–2024 was auto normalization. Used-auto delinquency started climbing. New-auto loan volume decelerated. The deployment engine that had carried many credit unions through the high-rate years started showing stress on both sides of the underwriting book.

Deposit Mix Shift, 2020 vs 2025

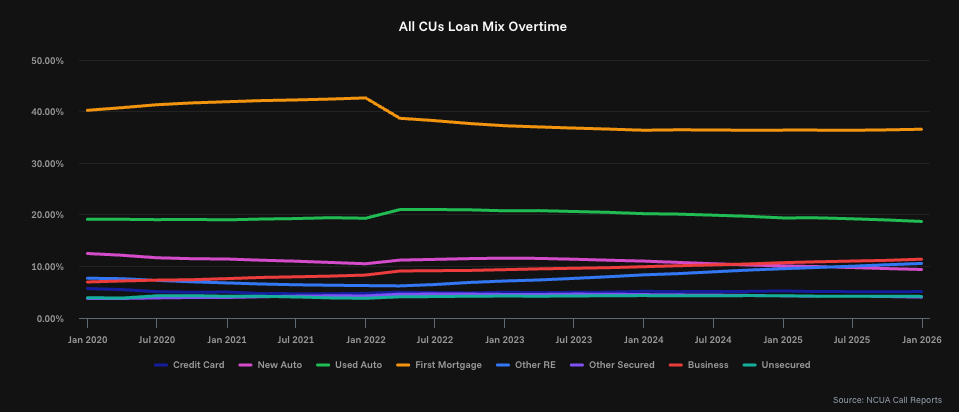

Loan Mix Shift, 2020 vs 2025

Two engines were critical to fast asset growth, and three cohorts emerged from how credit unions ran them.

Cert-First credit unions won the funding engine. They aggressively priced share certificates through the rate shock, locked in deposit growth, and built deposit franchises that compounded through 2022–2024. On the loan side, the mix is tilted toward first mortgage and away from the higher-margin, higher-velocity categories that drive return on assets. They maintained high asset growth throughout the period but had the lowest net interest margins of any playbook.

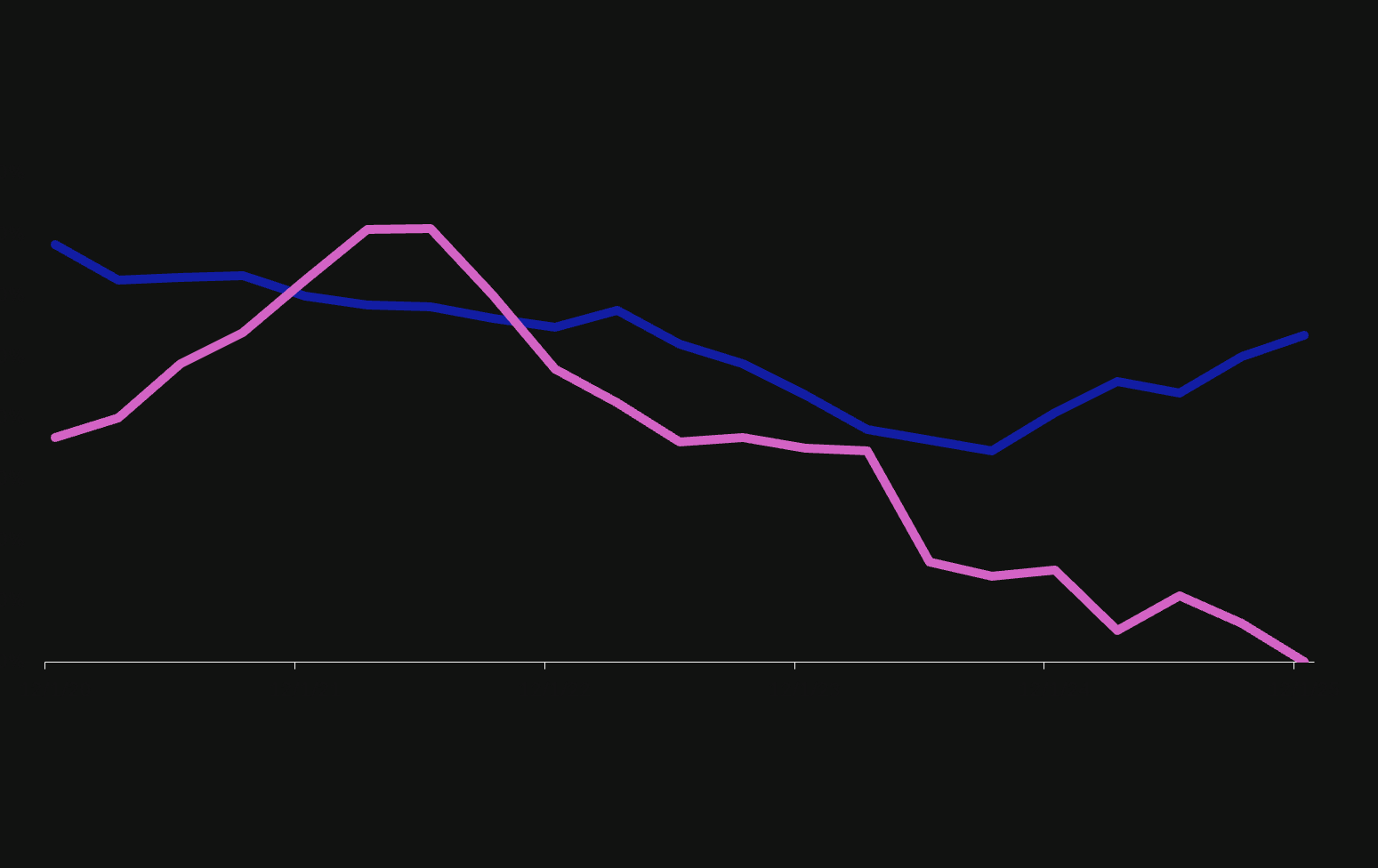

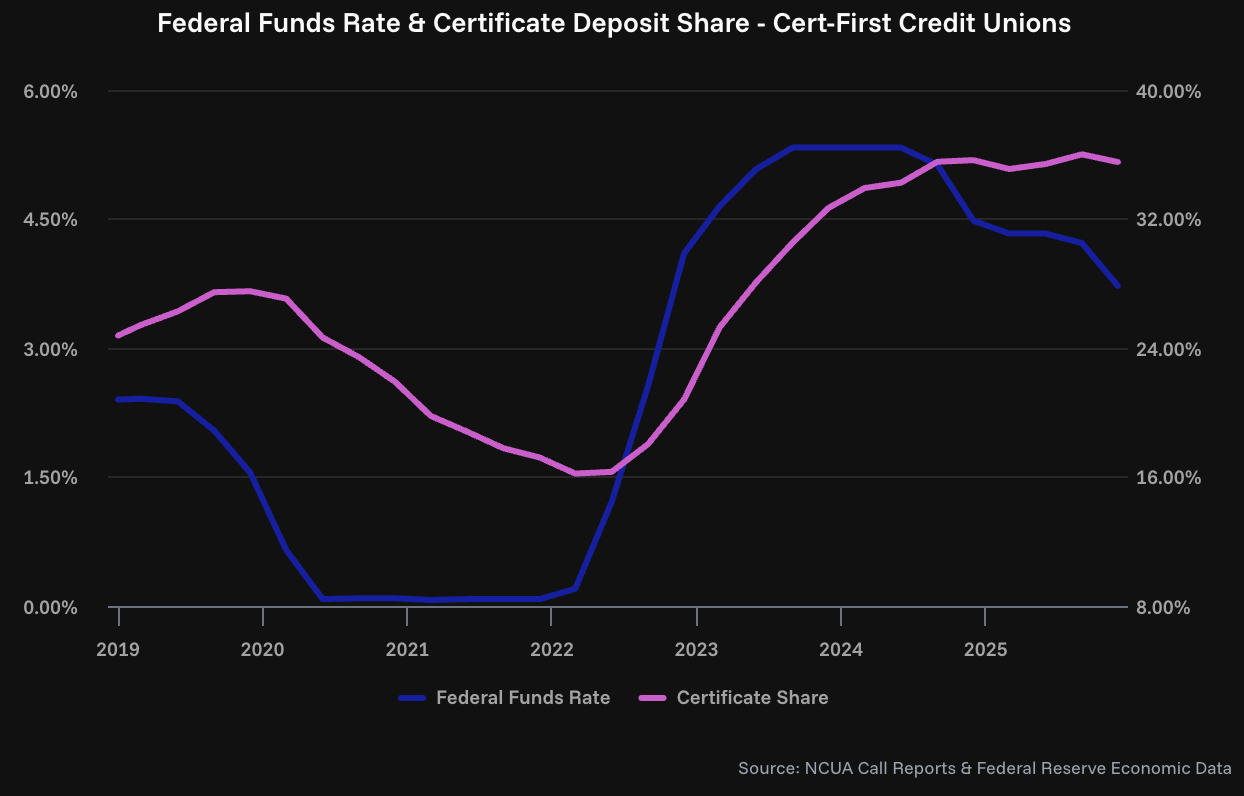

Share of Certificates & Federal Funds Effective Rate (2019–2025)

Auto-First credit unions ran the opposite engine. They built indirect channels, scaled used-auto books, and grew assets on the deployment side, without ever building the funding muscle to match. The auto-first credit unions suffered negative asset growth with the combination of the auto market normalization and the rate shock, however, rebounded to grow assets over 5% in 2025.

Fast Growers ran both engines simultaneously and grew assets at roughly 11% CAGR from 2020 through 2025. Slow Growers ran neither and shrank at -1% CAGR.

Cohort CAGR Matrix (2020–2025)

Four structural trends, the credit unions that take advantage will gain structural advantages.

Auto lending is under pressure on both sides. Used-auto delinquency continues to climb. New-auto loan volume is decelerating across the industry. Used-auto loans have been a particular growth center over last 5 years, growth likely slows if interest rates increase, but likely increases if interest rates decrease.

How rate changes affect Cert-First Credit Unions. The strategy that won 2022-2024, more certificate of deposits and riding the spread, is one that’s only viable in high-interest rate environments. It will face stresses as rates decrease. Between Q2 2019 and Q2 2020, the Federal Funds Target Range went from 2.25%-2.50% to 0.00%-0.25%, ushering in the low-rate covid environment. At the same time, certificate share went from 28% of Cert First CU Deposits to 16%. This precedent suggests with a decline in interest rates, certificate share of deposits will experience a large decline, as member preferences switch to products like money market funds.

However, if rates do not experience a decrease, Cert-First Credit Unions will continue to have a robust engine.

Member acquisition is now the most fragile engine in the industry. This is the trend that doesn't get enough attention. According to NCUA's Q4 2024system performance data, every asset tier below $1B saw aggregate membership decline last year, and the smaller the tier, the steeper the decline. Tiers under $100M lost 6–7% of their membership in a single year. Only credit unions above $1B grew members. The"$1B line" is now the dividing line between the part of the industry that's still acquiring and the part that's shrinking.

The $1B Line: Membership Growth by Asset Tier, 2024

And even the credit unions that are growing aren't growing the way the industry assumes. Assets per member have continued to rise across every tier, meaning the growth that's happening is coming from deepening existing relationships, not acquiring new ones. Even Fast Growers, the cohort that outperformed on every other metric, grew assets materially faster than they grew members.

Digital-first competitors are accelerating into the deposit market. Chime,SoFi, Cash App, and the regional digital banks are growing deposits at multiples of the credit union industry rate. These competitors leverage technology to provide strong customer experiences, oftentimes with radically different cost-structures.

Two lines, indexed to 100 at 2020.Credit unions are losing the deposit war to digital-first competitors.

At GAC last week, Filene named tenstrategic priorities for credit unions in 2026. Five of them, scale,differentiation, modern data strategy, deepening relationships, leveraging AI,describe the symptoms of an industry trying to run three engines without namingthem. One priority that should have made the list didn't: relationship preservation. We'll get to why thatone matters most.

The last 5 years ran on two engines.The next need three: Acquire, Grow, Retain. Each tied to a specific finding from our analysis of 4,015 credit unions. Each addressable. Each measurable.

Acquire: net new members at the front of the funnel. Member acquisition is the most under-leveraged engine in the industry today. Every tier below $1B is in aggregate decline. Even Fast Growers grew assets faster than they grew members.The industry has been compounding by deepening, not acquiring. Year-over-year membership growth is the only growth driver that ranks top-3 at every asset tier in our XGBoost analysis, and it's the metric decelerating fastest. The acquisition engine is about scoring every household in your field of membership for similarity to your best existing members, then giving your marketing and retail teams a ranked, addressable list to work this week, not a ZIP code blast or a purchased file. Smallest annual bucket of the three at a typical $1B+ credit union. Fastest-compounding lever over a five-year horizon.

Grow: relationship depth across the existing base. Accounts per Member is the #1 growth driver under $500M in our XGBoost analysis. Non-interest Income Ratio is the #1 driver at $1B+. Both are expressions of the same motion: deepening relationships with members you already have. Most credit unions have a member distribution heavily concentrated at one product per member. Fast Growers have shifted that distribution rightward. and they're doing it in a specific direction. Between 2020 and 2025, Fast Growers rotated their loan book out of consumer first mortgages (down 5.2 points)and into business lending and commercial real estate(up 7.7 points combined). The Grow engine is the cross-sell motion that moves your member-level product distribution, and the next phase of it is commercial.

Accounts per Member Distribution

Grouped bars. Typical $1B CU vs FastGrower benchmark across 1 / 2 / 3+ products per member. Fast Growers have shifted the distribution rightward.

Retain: relationship preservation across members, deposits, and loans. This is the engine the industry has the least language for, and it's the largest of the three at a typical $1B+ credit union. A strong defense is often the best offense, as credit unions not only compete against one another, but on external industries as well.

The credit unions that are able to build these engines and scale them the most effectively, will be in a position to adapt to the rapidly changing environment

Perspective for credit union leaders navigating growth, technology, and member strategy.